2021

Activity

The activities of STIFA focus on the supervision of common-benefit foundations and establishments as well as private-benefit fThe activities of STIFA focus on the supervision of common-benefit foundations and establishments as well as private-benefit foundations and establishments that have voluntarily submitted to supervision. Unless the entity is exempted from the obligation to appoint an auditor, STIFA receives an annual audit report on the proper management and use of the assets for its supervisory purposes. These reports are processed by STIFA and, if necessary, regulatory measures are requested from the Princely Court of Justice. In the case of foundations and establishments that are exempt from the obligation to appoint an auditor, STIFA normally carries out audits itself every three years. Furthermore, STIFA’s remit also includes checking the accuracy of the filed notifications of formation and amendments in the event of private-benefit foundations not entered in the Commercial Register.

Supervised entities

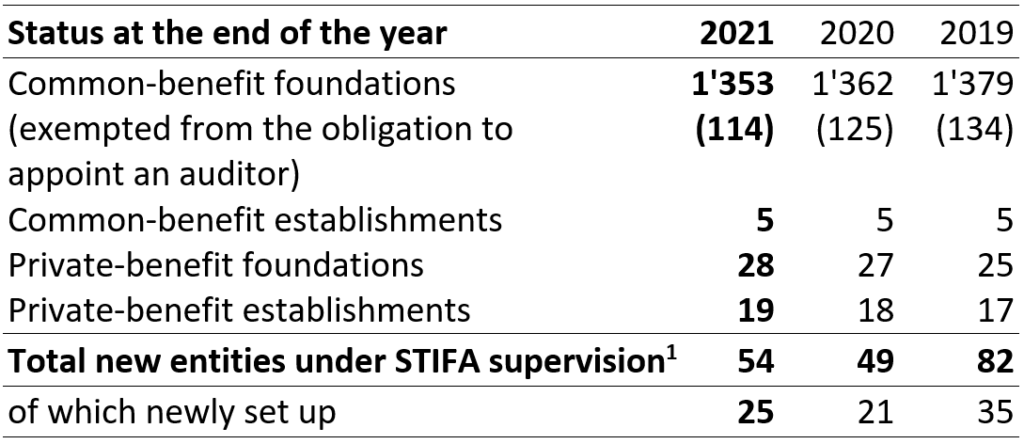

1 These numbers include common-benefit and private-benefit foundations and establishments.

Besides the 54 foundations and establishments that came under supervision for the first time in the year under report, 38 supervised foundations were put into liquidation, two were released from the supervision of STIFA and 59 were removed from the Commercial Register. The decline in the number of common-benefit foundations recorded for the first time in 2019 thus continued in the year under review (reduction of 0.7 % compared to the previous year). The number of common-benefit foundations that came under supervision of STIFA for the first time is thus lower than the number of terminations. It can be noted that the number of terminations in the year under review has slightly decreased compared to the previous year, while the number of common-benefit foundations newly placed under supervision of STIFA has comparatively increased slightly.

Proceedings concerning auditors

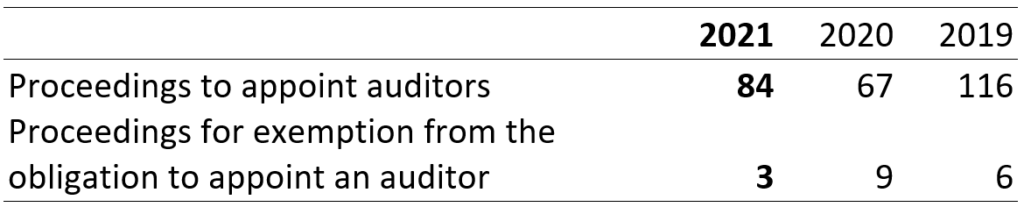

During the year under review, 84 foundations and establishments applied to the Princely Court of Justice for statutory auditors to be appointed. This also includes those proceedings in which an application was made for the replacement or dismissal of auditors. STIFA was a party to each of these proceedings. During the year under review, three common-benefit foundations applied to STIFA to be exempted from the obligation to appoint an auditor (Art. 552 § 27 Para. 5 PGR).

Audits conducted by the auditors

On 31 December 2021, 106 (previous year 83) audit reports relating to the financial year 2020 were still outstanding. This means the above stated number of objections and referrals relating to the audited 2020 financial year will increase slightly until the reports have been submitted in full.

With regard to the objections raised by auditors relating to the 2020 financial year, it should be noted that these were largely due to improper use of the assets, in particular due to the lack of distributions over a longer period of time. Furthermore, organisational shortcomings (e.g. lack of approval by foundation bodies to resolutions, non-compliance with investment guidelines) also led to objections.

With regard to the referrals made by auditors concerning the 2020 financial year, the picture is broadly similar, namely that a large proportion of the matters requiring notification related to deficiencies in distribution practice. A large number of referrals were also made for the purpose of informing STIFA about pending legal proceedings or about an accounting over-indebtness pursuant to Art. 182e and Art. 182f PGR.

STIFA has examined the objections and referrals identified by the auditors and has taken the necessary measures.

Audits conducted by STIFA

In the case of foundations and establishments that are exempt from the obligation to appoint an auditor (by the end of 2021: 114), STIFA normally carries out the audit itself every three years. STIFA subjected a total of 34 (45 in the previous year) common-benefit foundations to an independent audit during the year under review, whereby these audits were carried out by correspondence, analogous to the previous year, due to the Covid-19 pandemic.

On 31 December 2021, eleven audits of STIFA were still pending. This means the above stated number of objections and referrals will increase slightly until the audits of STIFA have been completed in full.

With regard to the objections and referrals ascertained by STIFA, it should be noted that the picture is broadly analogous to the objections and referrals made by the auditors. The findings were mainly made due to the improper use of the assets of the foundation, in particular the lack of distributions over a longer period of time, as well as organisational shortcomings (i.e. lack of documentary evidence of disbursements received). In addition, as in the previous year, STIFA increasingly highlighted the disproportionately high costs of foundation management. Furthermore, STIFA revoked the exemption from the obligation to appoint an auditor for three foundations, as a reliable assessment by STIFA of the ultimate use of the assets was not possible.

STIFA took the necessary measures based on the objections and referrals identified.

Supervisory proceedings and other proceedings

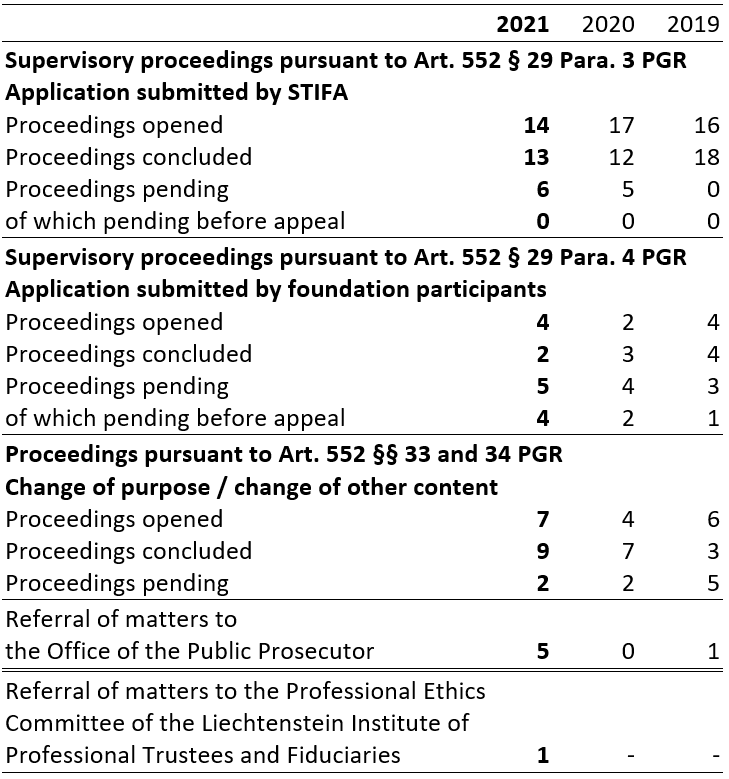

In 14 cases STIFA applied to the Princely Court of Justice for supervisory measures during the year under review (Art. 552 § 29 Para. 3 PGR). In addition, in four instances foundation participants applied to the Princely Court of Justice for supervisory measures to be taken against foundations and establishments subject to STIFA supervision (Art. 552 § 29 Para. 4 PGR). STIFA was a party to each of these cases.

Furthermore, in the year under review STIFA was asked to make statements in seven cases on account of its party status in respect of changes to the purpose and other contents of the foundation documents, in particular the organisation, that had been requested at the Princely Court of Justice (Art. 552 § 33 and 34 PGR).

In addition, In the year under review, STIFA reported five cases to the Office of the Public Prosecutor on suspicion of criminal offences and one case to the Professional Ethics Committee of the Liechtenstein Institute of Professional Trustees and Fiduciaries on suspicion of possible violations of the Code of Professional Conduct.

Audits of formation and amendment notifications

In the case of a total of 22 representatives, the accuracy of the notifications of formation and amendments of private-benefit foundations not entered in the Commercial Register (Art. 552 § 21 PGR) was verified on a random basis during the year under review.

With regard to the total of 147 foundations audited, STIFA was informed of the following objections and referrals by the appointed auditors:

- In the case of 12 foundations, STIFA was notified of referrals due to organisational deficiencies. These deficiencies were of a purely formal nature and did not require any further action on the part of STIFA.

- In the case of four foundations, STIFA was informed that notifications of amendments had not been filed with the Commercial Register within the statutory period of 30 days. Since these notifications of amendments were submitted late, but nevertheless were made, no measures were necessary or possible by law with respect to these objections.

- In the case of one foundation, it was found that the foundation had a common-benefit purpose, but that it was not registered in the Commercial Register and was not subjected to STIFA supervision. As the foundation in question had already been deleted at the time of the audit and since its formation had no assets except for the minimum capital, no measures were necessary due to the notified objection.

- In the case of one foundation, it was found that the purpose did not comply with the so-called requirement of certainty. However, the purpose could be corrected on the basis of the available documents and the foundation council’s right to make amendments.

- In the case of two foundations, STIFA was informed that it was unclear whether they were common-benefit foundations and thus subject to supervision. In addition, it was found that for one of these two foundations, the purpose entered in the Commercial Register did not correspond to the purpose stipulated in the statutes. STIFA has asked the foundation concerned to state their position and will initiate further measures based on this if necessary.